Table of Contents

Cyber Insurance AI Denial: Why Shadow AI Costs You the Claim

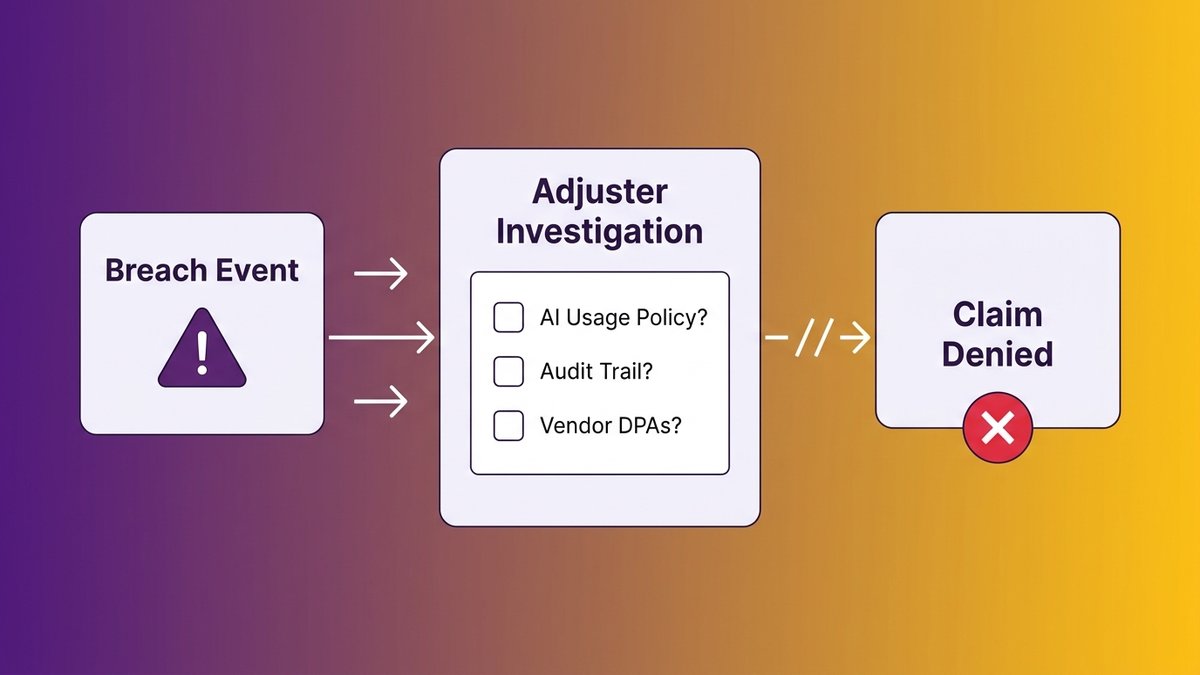

Your company gets breached. Customer data is exposed. You file the cyber insurance claim you’ve been paying for. Then the adjuster asks one question: can you show us your AI usage policy and the audit trail proving your employees followed it?

You can’t. Neither can most mid-market companies right now. The claim gets denied.

Cyber insurance AI denial is no longer hypothetical. Insurers are rewriting underwriting criteria in 2026, and AI governance documentation has become a primary signal during both renewals and claim investigations. A breach that would have paid out last year may not pay out this year, not because the breach was worse, but because shadow AI activities were present and undocumented. For a 200-person company, that gap can mean the difference between recovering and not.

What insurers now examine during a claim: AI governance documentation, audit trails, and usage policy compliance records alongside traditional breach evidence.

The Claim Your Policy Won’t Cover

Insurance denial rarely announces itself as “you used AI wrong.” It arrives in policy language, a clause about “reasonable security controls,” a “failure to document preventative measures” exclusion, or an explicit AI usage rider added at renewal without anyone noticing. By the time you’re reading the denial letter, the breach has already happened.

When governance documentation is the missing piece

The mechanism works like this. A data breach occurs, and the investigation reveals that an employee pasted customer records into a consumer AI tool to generate a report. That tool’s privacy policy allowed training on user inputs. The insurer has grounds, not necessarily because the policy says “we won’t cover AI,” but because the absence of any governance documentation signals a failure in the security controls your application certified you maintained.

Cyber insurance applications ask you to certify your security posture. You tick the boxes: multi-factor authentication, endpoint protection, incident response plan, employee security training. You don’t tick a box labeled “unsanctioned AI usage policy” because that box doesn’t exist yet on most applications. But when a breach investigation surfaces that employees were routing sensitive data through unmonitored consumer AI platforms, the adjuster can argue that your certified security controls were incomplete.

The documentation gap is the primary denial trigger. Insurers aren’t denying claims because AI was used. They’re denying them because policies were absent, audit trails didn’t exist, and no one could reconstruct what data went where.

Why mid-market companies are disproportionately exposed

A Fortune 500 company has a full-time CISO, a legal team that reviews every policy renewal, and an IT department that audits software provisioning. Your 200-person company has a shared IT director, a CEO who signs the insurance renewal after a 10-minute review, and operations teams who figured out that ChatGPT is faster than the internal reporting tool nobody updated in three years.

That’s not a failure of character. It’s a structural exposure that affects mid-market companies specifically. Enterprise companies have governance infrastructure. Small companies fly under the radar on size alone. Mid-market companies sit in the worst position: large enough to carry significant sensitive data, small enough to lack the governance layer insurers now expect to see documented.

Shadow AI Is Not a Security Team Problem, It’s an Operations Problem

Your operations teams didn’t adopt ChatGPT or Perplexity because they wanted to create a compliance problem. They adopted them because your internal tools couldn’t do what they needed fast enough. Shadow AI enters through workflow gaps, not IT failures. That distinction determines who owns the fix.

How unsanctioned AI tools enter through workflow gaps, not IT failures

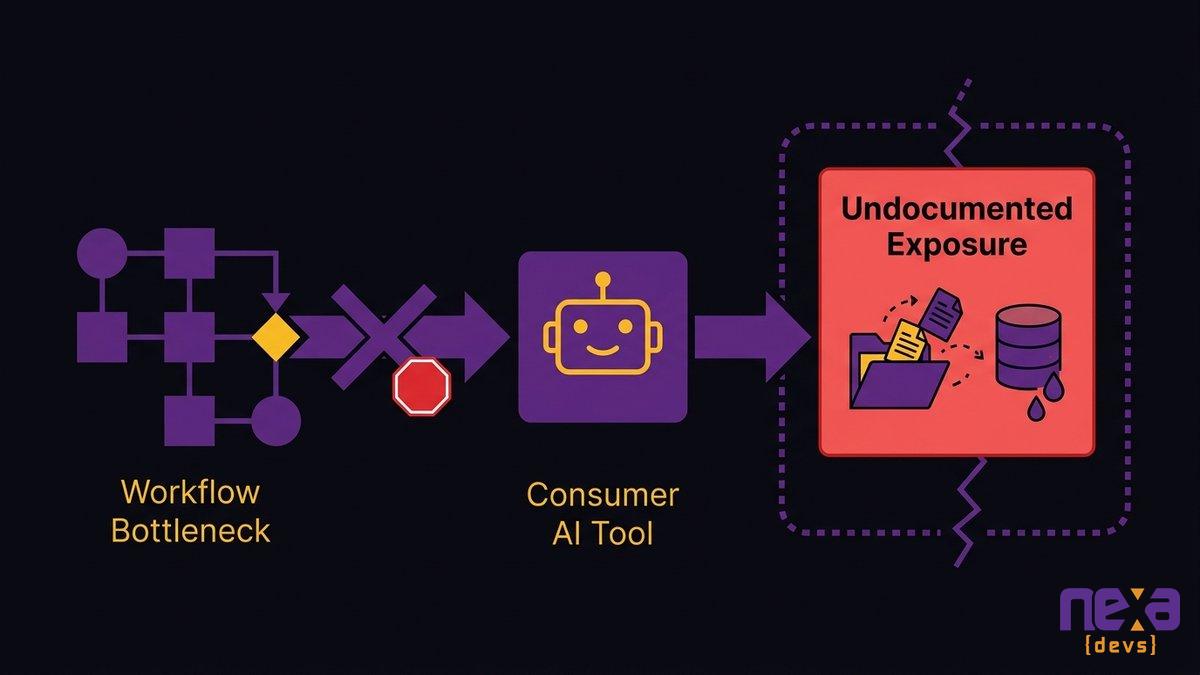

Picture your finance coordinator. She needs to summarize 40 vendor contracts before a board meeting. The internal document management system is slow, the search function is broken, and the vendor locked you out of the AI feature unless you upgrade your plan. She opens a consumer AI tool, pastes the contract text, and gets the summary she needs in 90 seconds.

No malicious intent. No policy she was aware of violating. No record in any system that vendor contract data, which may include pricing terms, payment clauses, and third-party obligations, just passed through a consumer AI model with a data retention policy your legal team has never reviewed.

That’s the shadow AI story in most mid-market operations. Not a rogue employee. Not an IT failure. A workflow gap that a consumer AI tool filled faster than anyone anticipated.

Gartner’s 2023 cybersecurity predictions put the trajectory plainly: by 2027, 75% of employees will acquire, modify, or create technology outside IT’s visibility, up from 41% in 2022. The consumer AI wave accelerated this curve faster than almost anyone predicted.

The typical shadow AI entry path: an operations workflow bottleneck leads an employee to a consumer AI tool, creating an undocumented data exposure point outside IT visibility.

The difference between shadow IT and shadow AI (and why shadow AI scales faster)

Shadow IT has existed for decades. The finance team installs Dropbox. Marketing subscribes to a SaaS tool IT didn’t approve. IT eventually discovers it, evaluates it, and either sanctions or removes it. The risk surface is proportional to the number of users.

Shadow AI works differently. A single employee who builds a workflow using an AI tool can expose thousands of customer records in one session. The risk surface isn’t proportional to users. It’s proportional to what the tool processes. A finance analyst running a revenue model through an unapproved AI platform isn’t one person’s risk. It’s your entire customer financial dataset’s risk, processed without an audit trail, by a vendor whose data handling practices you’ve never reviewed.

CIO Dive’s reporting on Torii’s 2026 SaaS Benchmark Report found that only about 15% of discovered applications in enterprise environments are fully sanctioned by IT, with more than 61% lacking formal approval or oversight. AI tools accelerate this ratio because the barrier to adoption is effectively zero.

What Insurers Are Actually Looking for During Renewals

Renewal questionnaires have changed. The prior year’s version asked about firewalls, MFA, and patch management. This year’s asks about AI. Most mid-market CEOs are answering those questions without fully understanding what the underwriter is scoring.

AI governance documentation as an underwriting signal

When underwriters ask about AI, they’re looking for three things. Do you have a written AI usage policy naming approved tools, data access rules, and enforcement ownership? Do you have an audit mechanism, any documented mechanism, for identifying what AI tools are in use? And do you have data processing agreements with the AI vendors whose tools your employees use?

Companies that answer “we’re working on it” to all three are underwriting liabilities. Some insurers are declining to renew. Others are adding specific exclusions. Premiums are rising for organizations that can’t demonstrate a basic AI governance posture, and that shift is independent of whether you’ve actually had a breach.

The new exclusions appearing in cyber policy language

AI-related exclusions are showing up more frequently in 2026 policy renewals. The form varies, but the consistent pattern is an exclusion for losses arising from the use of unsanctioned or unreviewed AI tools that processed the affected data. If your breach involved shadow AI and your policy has this language, that exclusion is the mechanism that denies your claim, even if your overall policy covers ransomware and data breach events broadly.

Read your current policy. Look for language about “approved technology,” “sanctioned systems,” or “authorized third-party services.” The exclusion may already be there. SentinelOne’s May 2026 cyber insurance analysis notes that insurers have begun adding specific exclusions for shadow AI activities and related liabilities. This is a directional shift, not a universal standard yet, but the direction is clear.

What “AI usage policy” means in practice for a 200-person company

You don’t need a 40-page governance framework. A two-page policy that names approved tools, specifies data handling rules, assigns ownership, and establishes a review cadence is more defensible than a sophisticated framework that’s 14 months out of date. The bar isn’t perfection. The bar is documentation.

Insurers are not grading the quality of your AI governance program. They’re confirming it exists. A documented policy, even a simple one, communicates something the absence of any policy cannot: that someone at your company thought about this problem and acted on it.

The Compliance Landscape: What Regulations Now Require

The regulatory picture on AI governance is genuinely in motion right now, and mid-market CEOs are getting conflicting signals. Some advisors are still citing a hard compliance deadline this summer. That framing is no longer accurate.

Colorado AI Act: what the amendments and enforcement stay mean for your timeline

Colorado passed SB 24-205 in 2024. Known as the Colorado AI Act, it was one of the first state-level AI governance laws in the United States. The original law carried a compliance deadline that generated significant urgency in early 2026 advisor communications.

A federal judge stayed enforcement in April 2026. The Colorado legislature then amended the law in May 2026 with revised terms and extended effective dates. This is corroborated by law firm publications from Hunton Andrews Kurth, Norton Rose Fulbright, and Skadden, as well as Colorado legislative records. The June 30 hard deadline that circulated widely in May briefings is not current.

What hasn’t changed: the governance documentation requirements the Act was designed to address remain real compliance expectations, and other regulatory frameworks are moving in the same direction. The enforcement stay gives you more time than you had in May. It doesn’t reduce the underlying governance gap. An insurer asking for your AI governance documentation at renewal doesn’t care about the Colorado enforcement calendar.

Where other state and federal AI governance requirements stand

Colorado isn’t alone. Multiple states have advanced AI governance legislation, and federal regulatory agencies have issued guidance affecting AI use in financial services, healthcare, and consumer-facing applications. The consistent thread across all of them is documentation: written policies, impact assessments, audit trails.

The specific law that applies depends on your industry, your customers’ locations, and the nature of decisions your AI tools influence. That legal analysis belongs with your general counsel. What belongs on your desk right now is the documentation foundation: written policy, audit mechanism, vendor data processing agreements. Those are required regardless of which jurisdiction you’re reading.

The documentation floor every mid-market company needs regardless of jurisdiction

Across every regulatory framework and every current underwriting questionnaire, the documentation floor is consistent. A written AI usage policy. An inventory of AI tools in use, sanctioned and discovered. Data processing agreements with every AI vendor handling personal or sensitive data. An internal audit or monitoring mechanism, even a basic one. A policy review cadence, even annual.

That list isn’t a compliance checklist. It’s the minimum documentation set that prevents a governance argument from being the reason your claim gets denied.

Auditing Your Shadow AI Exposure: A Starting Point for Operations Leaders

You can’t govern what you haven’t found. The audit isn’t an IT project; it’s a half-day operations exercise that produces a ranked list of your actual exposure.

A shadow AI audit maps unsanctioned tool usage across operational workflows to identify data exposure points before an insurer or regulator does.

Where to look: the most common unsanctioned AI entry points in mid-market ops

Start with the workflows that carry the most pressure and the least tooling. In most mid-market operations, those are: customer-facing communications, financial reporting and data aggregation, HR processes involving personal data, document processing and summarization, and any function where the primary tool is a spreadsheet with a chronic bottleneck.

Ask each department head three questions. What AI tools is your team currently using, in any form? What types of data does your team routinely work with? If someone needed to summarize or analyze that data quickly, what would they use today? You’ll capture most of the shadow AI picture from those answers without involving IT forensics.

The IBM 2025 Cost of a Data Breach Report found that 97% of organizations that suffered an AI-related breach lacked proper AI access controls, and shadow AI was present in 20% of those incidents. The access control gap is almost always upstream of the breach. Discovering it through an internal audit costs far less than discovering it through a claim denial.

What to document: the minimum audit trail insurers require

Once you know what tools are in use, document five things for each: the tool name and vendor; the data categories processed through it; whether that processing was known and approved or discovered during the audit; whether a data processing agreement exists with the vendor; and the action taken, whether that’s continued use under new policy, discontinuation, or pending review.

That log is the artifact an adjuster will ask for. It’s not a penetration test. It’s a list showing you know what’s running in your business and have assessed the risk, which is exactly what the underwriter needs.

Why Banning AI Tools Doesn’t Solve the Coverage Problem

Blanket AI bans are the instinctive response and the wrong one. They don’t eliminate shadow AI usage. They push it further underground, to personal devices, to tools accessed outside the corporate network, to use patterns that are genuinely invisible to your security stack.

Bans drive usage underground, and underground usage is undocumented

A policy that prohibits AI tool usage without a sanction process assumes employees will choose inefficiency over productivity. They won’t. Personal devices work, consumer platform accounts are free, and data keeps moving through tools that exist in a category your policy didn’t define clearly enough.

You’ll have a ban on paper and shadow AI everywhere else. Palo Alto Networks’ cybersecurity research confirms this pattern: visibility into actual shadow AI usage declines when organizations implement broad prohibitions rather than structured governance. You lose the ability to see what’s happening, which means you lose the ability to document it.

Underground usage is also harder to defend at claims time than governed usage that followed documented policy, even imperfectly. With a ban, you’re not eliminating the risk. You’re eliminating your visibility into it.

The governance model that satisfies both employees and underwriters

Documented and structured governance is the model that works. An approved tools list. A data classification rule that tells employees which data categories can and can’t be processed through AI systems. A simple intake process for requesting approval of new tools. An employee acknowledgment record.

Employees get to use AI tools that solve real workflow problems. Underwriters get documentation that governance existed. You get a coverage position that holds under scrutiny. The COO framing: structured governance doesn’t restrict what your team can do. It replaces the current situation where your team is doing whatever they want and you’re carrying the insurance exposure for all of it.

Custom Internal Tooling as the Coverage-Safe Alternative

The governance model handles the risk. Custom internal tooling removes the root cause. The distinction matters for how durable your solution actually is.

How purpose-built internal tools replace consumer AI tools with auditable alternatives

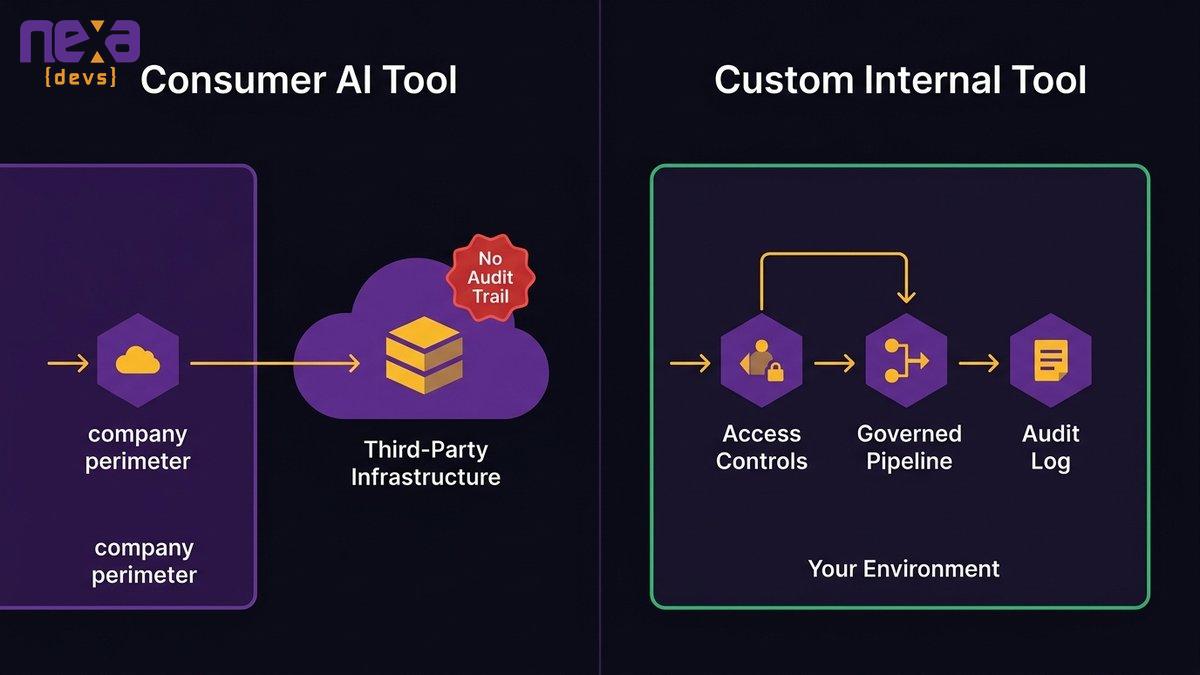

When employees use a consumer AI tool to summarize contracts because your internal systems don’t have that capability, the governance model patches the exposure. A custom internal tool that does contract summarization, built on a governed AI infrastructure, processing data within your environment, generating an audit trail by design, removes the exposure entirely.

The difference is architectural. Consumer AI tools process your data on someone else’s infrastructure under someone else’s data handling terms. Custom internal tools process your data in your environment under your terms, with operations logged, data access attributable, and every AI output traceable. “Auditable” means something specific to an underwriter: not that you watched your employees use the tool, but that the tool itself generates the audit trail.

Purpose-built internal software replacing manual workflows

What governance documentation looks like when AI is built into the workflow by design

When AI capability is built into an internal tool rather than accessed through a consumer platform, governance documentation emerges from the development process itself. Architecture documentation describes what data flows where. System design records capture what AI infrastructure is used and under what contractual terms. Access control records show who can use the tool and for what data categories.

None of that requires a separate compliance exercise. It’s a byproduct of building the tool correctly. The insurer’s documentation checklist is already satisfied before you file the renewal.

The operational case: solving the workflow problem that created shadow AI in the first place

Take the finance coordinator who needed to summarize 40 vendor contracts. Or the operations team extracting data from supplier PDFs. Or support trying to draft customer responses faster than the CRM’s template system allowed. Consumer AI tools solved all of those problems, outside your governance perimeter.

Custom internal tooling solves the same problems, with your data policies, your access controls, your audit trail, and your security architecture. The shadow AI risk disappears not because you banned the behavior, but because the behavior no longer needs to happen outside a governed system.

The COO gets the efficiency. The CEO gets the coverage position. One tool delivers both.

Purpose-built internal AI tools route data through governed, auditable infrastructure, generating the documentation trail that insurance underwriters require and consumer AI tools cannot provide.

What Your Insurer Wants to See Before Your Next Renewal

This section is for your general counsel, your COO, or whoever owns your insurance renewal process. These are the artifacts that underwriters ask for and claims adjusters require.

The AI governance documentation checklist

Before your next renewal, you should be able to produce:

- AI tool inventory: A list of all AI tools in use, including the date each was approved, the approving authority, and the data categories each tool is permitted to process. Include tools discovered during your shadow AI audit with their current status.

- Data classification policy: A written policy categorizing your data types (personal data, financial records, client data, proprietary information) and specifying which categories can be processed by AI tools and under what conditions.

- Employee training record: Documentation that employees were informed of the AI usage policy, including the date of training and acknowledgment records.

- Vendor data handling review: For each approved AI tool or platform, a record that you reviewed the vendor’s data processing terms and made a documented decision about acceptability.

- Incident response update: A version of your existing incident response plan that addresses AI-related data exposure scenarios, not just traditional breach scenarios.

- Named accountability: A role or individual designated as responsible for AI governance. This doesn’t require a new hire. It requires a name in a document.

How to communicate your AI posture to underwriters

Lead with what you’ve done, not what you intend to do. Underwriters’ weight completed controls significantly higher than planned controls. When your broker submits the renewal application, a one-page summary of your AI governance program (approved tools, data classification framework, audit mechanism, review cadence) submitted proactively signals that you’ve addressed the risk intentionally.

“We conducted a shadow AI audit in [month] that identified [N] unsanctioned tools. We discontinued [N], approved [N] under new data handling terms, and implemented an employee training process documented in the attached log.” That narrative, with artifacts attached, positions you as a company that identified and addressed a risk category. That’s the security posture cyber insurance is designed to reward.

Ready to replace unsanctioned AI tools with governed internal software built around your actual workflows? Talk to Nexa Devs about building coverage-safe AI tooling. We build auditable internal tools that solve the workflow problems that created shadow AI in the first place.

FAQ

Is AI covered under cyber insurance?

AI use itself isn’t excluded from most cyber policies, but breaches caused by unsanctioned AI tools can be. If an employee routes sensitive data through a consumer AI platform without documented governance, the insurer may deny coverage, citing failure to maintain reasonable security controls. The risk isn’t AI use. It’s undocumented AI use.

What are the most common reasons cyber insurance claims are denied?

Claims are most commonly denied for absent security controls, failure to document preventative measures, delayed breach notification, and third-party data processor oversight failures. In 2026, missing AI governance documentation has emerged as a newer denial basis as insurers update underwriting criteria and adjust breach investigations.

Does shadow AI affect cyber insurance coverage?

Yes. Shadow AI creates undocumented data exposure that insurers treat as a security control failure. When a breach reveals that employees used consumer AI tools without governance documentation, insurers have grounds to deny claims under existing exclusions. The documentation gap is the direct denial mechanism.

What controls improve underwritability for AI risks?

Underwriters look for an approved AI tool inventory, a data classification policy applied to AI use cases, employee training records, vendor data handling reviews, and a named governance role. These don’t require a compliance team. A completed documentation package signals that your security posture is active and managed.

How does shadow AI impact compliance in regulated industries?

In financial services, healthcare, and education, shadow AI creates dual exposure: insurance denial risk and regulatory violation risk. Data processed through consumer AI tools without governance can trigger breach notification obligations and compliance failures. The documentation requirements for cyber insurance renewals substantially overlap with regulatory documentation requirements.

What is the difference between shadow IT and shadow AI?

Shadow IT is any technology used without IT approval. Shadow AI is a faster-moving version: AI tools accessed through a browser with no installation, no network traffic to monitor, and no license purchase to flag. An employee can route sensitive data through a consumer AI platform on a personal device with no corporate system seeing it, making shadow AI a distinct insurance risk category.